The Digital Paradox: Balancing Innovation and Reliability in China’s Evolving NEV Marke

The Digital Paradox: Balancing Innovation and Reliability in China’s Evolving NEV Market

Executive Summary: A Critical Juncture for Quality

The Chinese New Energy Vehicle (NEV) market, widely recognized as the global epicenter of automotive electrification and digitization, has reached a defining moment of maturity. As the market transitions from early adoption to mass-market dominance, consumer expectations are undergoing a profound shift. The initial thrill of cutting-edge technology is increasingly being tempered by a demand for foundational reliability and seamless usability.

According to the latest findings from J.D. Power’s 2025 China New Energy Vehicle Initial Quality Study (NEV-IQS), the industry is grappling with a persistent and growing disconnect between technological ambition and execution. While significant strides have been made in alleviating range anxiety—historically the primary barrier to NEV adoption—new fissures have emerged in the digital experience and the structural integrity of increasingly complex powertrains.

The 2025 study, based on feedback from 20,829 owners who purchased vehicles between July 2024 and January 2025, reveals that while the industry is stabilizing, it is still trending toward higher problem rates. The industry average for initial quality stood at 226 problems per 100 vehicles (PP100)—a metric where a lower score reflects higher quality. This represents an increase of 16 points from 2024. However, there is a silver lining: the rate of quality deterioration has slowed significantly compared to the previous year’s precipitous 37-point jump, suggesting that manufacturers are beginning to arrest the slide, even if they have not yet reversed it.

This report integrates the findings across powertrain segments, specific problem categories, and strategic market shifts to provide a holistic view of the quality challenges facing China’s automakers in 2025.

Part I: The Information Entertainment Crisis

The "Smart" Cockpit’s Usability Struggle

The most glaring finding of the 2025 NEV-IQS is the status of the Information Entertainment System (Infotainment). For years, Chinese automakers have differentiated themselves through "smart cockpits"—cabins laden with massive screens, voice assistants, and connected ecosystems. However, the data suggests that this aggressive digitization has become a double-edged sword.

In 2025, Infotainment remained the single most problematic category among the ten evaluated, generating 31 PP100. This figure identifies the digital interface as the primary source of owner dissatisfaction, overshadowing mechanical issues, exterior flaws, or powertrain concerns. The specific complaints cited by owners paint a picture of friction rather than fluidity:

Touchscreen Responsiveness: Delays and lack of sensitivity in high-definition screens.

Voice Recognition Accuracy: Failures to understand natural language commands, a critical feature in button-less cabins.

Connectivity Failures: Issues with Bluetooth, 5G linking, and app integration.

UI/UX Inconsistency: Confusing menu structures that bury essential functions under layers of digital complexity.

The Ripple Effect: Control Systems Under Pressure

The issues with infotainment are not isolated; they are spilling over into adjacent systems. The study notes that the Configuration/Control/Cluster Systems category witnessed the largest year-over-year increase in complaints, rising by +3.5 PP100.

This correlation is not coincidental. As automakers race to integrate "minimalist" interiors by migrating physical buttons to digital touchscreens, the reliability and intuitiveness of fundamental controls have suffered. Drivers are finding it increasingly difficult to perform basic tasks—such as adjusting mirrors, climate control, or drive modes—because these functions are now tethered to the very infotainment systems that are prone to glitching.

J.D. Power analysts describe this phenomenon as a "strategic imbalance." In the rush to win the "screen wars," manufacturers have prioritized eye-catching specifications over robust, user-centric engineering. The result is a generation of vehicles that look futuristic in the showroom but feel beta-tested on the road.

Part II: The Powertrain Divergence

BEVs vs. Hybrids: A widening Quality Gap

One of the most significant trends identified in the 2025 study is the divergence in quality performance between Battery Electric Vehicles (BEVs) and hybrid architectures, specifically Plug-in Hybrid Electric Vehicles (PHEVs) and Extended-Range Electric Vehicles (EREVs).

While BEVs maintained a relatively better quality score of 220 PP100, both hybrid categories significantly underperformed the industry average:

PHEVs: 234 PP100

EREVs: 235 PP100

This gap of 14–15 points highlights the inherent challenges of complex engineering. Unlike BEVs, which benefit from the simplicity of electric motors, PHEVs and EREVs must integrate two distinct propulsion systems (internal combustion and electric) along with complex transmission or energy generation mechanisms. As these segments experience explosive sales growth—particularly in the mass-market 10–30万元 (100,000–300,000 RMB) price bracket—quality control appears to be straining under the pressure of scale.

The Anatomy of Failure: Design vs. Defects

The study provides a granular breakdown of why these hybrid vehicles are failing, revealing distinct stress points for each technology:

1. PHEVs: The Design Dilemma

Plug-in Hybrids saw a sharp +12 PP100 increase in design-related issues. This suggests that the problems are not necessarily manufacturing defects (things breaking), but rather poor engineering choices or compromises made during the development phase. As legacy automakers and new entrants rush to retrofit platforms or develop widespread hybrid solutions to meet emission targets and consumer demand, fit-and-finish, ergonomic integration, and packaging seem to be suffering.

2. EREVs: The Reliability Risk

In contrast, Extended-Range vehicles (where a gas engine acts solely as a generator) experienced a +17 PP100 rise in fault/malfunction-related problems. This is a more concerning metric, as it indicates actual system failures rather than just user dissatisfaction with design. The complexity of managing the thermal and mechanical interplay between the range-extender (engine) and the electric drive system is proving difficult to perfect at mass-production speeds.

The Software Burden on Hybrids

The complexity of hybrid vehicles also exacerbates digital issues. Infotainment complaints rose by +5 PP100 for PHEVs and +7 PP100 for EREVs. Even more alarming was the performance of Driver Assistance Systems (ADAS) in EREVs, which saw a surge of +6 PP100 in complaints. This suggests that the computing power required to manage the dual-powertrain architecture might be diverting resources or stability from the ADAS and infotainment stacks, leading to a less stable overall electronic architecture.

Part III: The Bright Spot – Battery Engineering

The End of Range Anxiety?

Amidst the rising tide of complaints regarding software and hybrid complexity, there is one resounding success story in the 2025 NEV-IQS: Battery and Charging.

This was the only problem category to show a statistically significant improvement, declining by 3.2 PP100. For the past decade, "range anxiety" and "charging failures" were the dominant narratives in the EV market. The 2025 data indicates that this chapter is closing.

The reduction in complaints is attributed to:

Matured Cell Chemistry: Advancements in energy density and stability.

Better BMS (Battery Management Systems): More accurate range estimation algorithms that align displayed range with actual driving performance.

Infrastructure Compatibility: Improved "handshakes" between vehicles and public charging stations.

This progress serves as a crucial proof of concept for the industry. It demonstrates that focused, rigorous engineering efforts can resolve core consumer anxieties. The industry has successfully "solved" the hardware challenge of the battery; the question now is whether they can apply that same rigor to the software challenge of the cockpit.

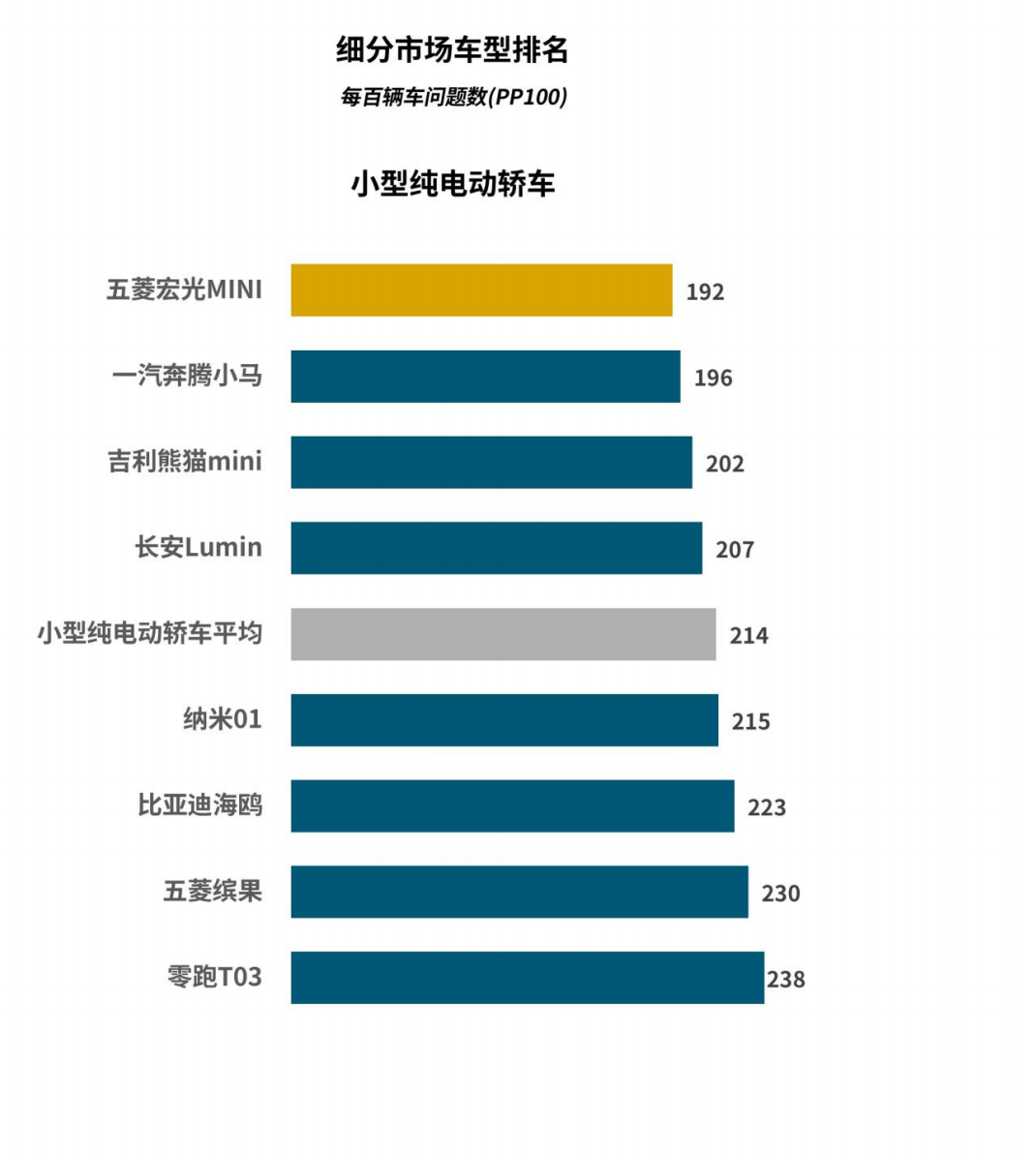

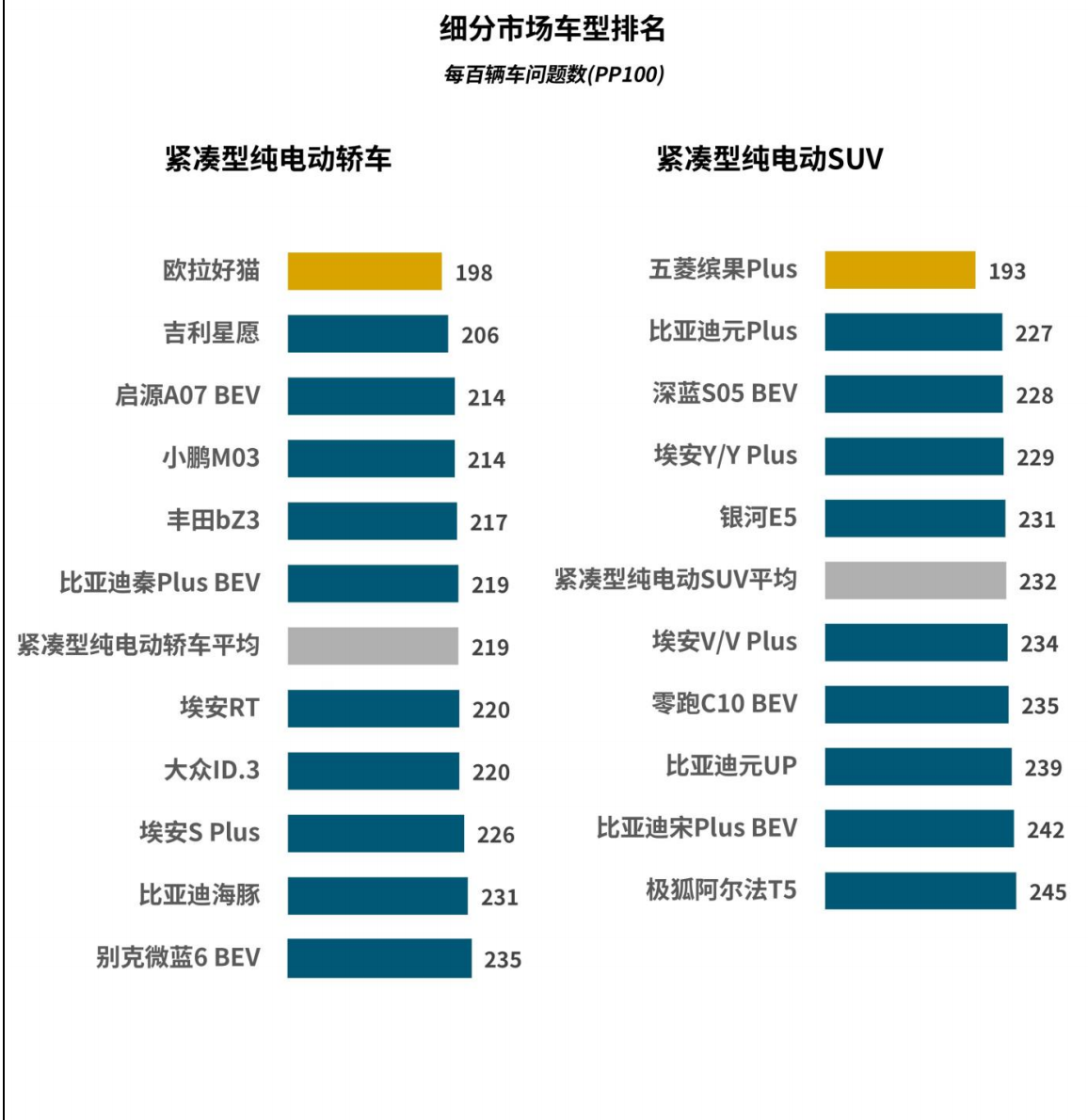

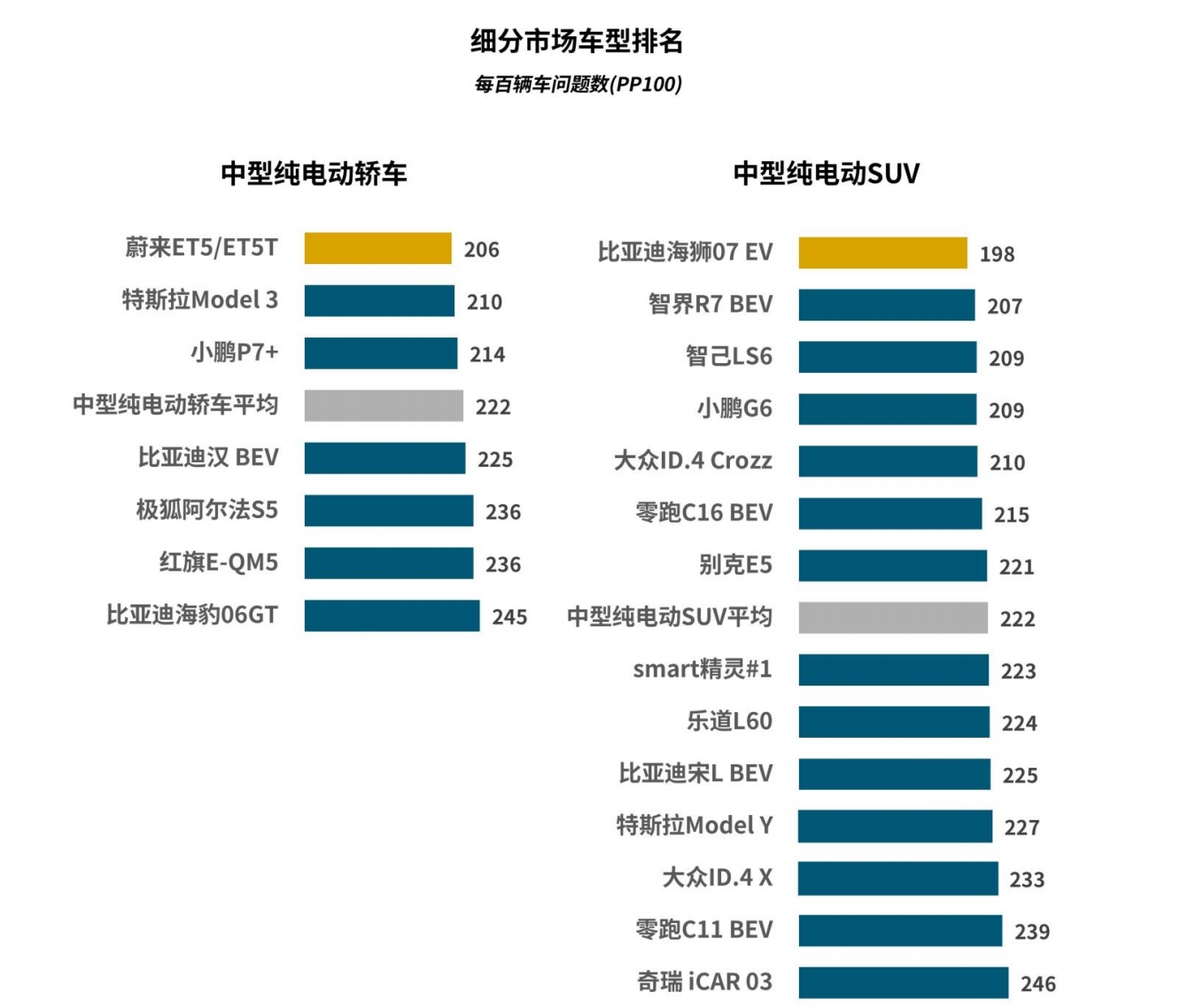

Part IV: Market Segmentation and Consumer Trends

The "Boxy" SUV and Lifestyle Trap

The 2025 market landscape is defined by the rise of "lifestyle" vehicles—specifically MPVs and off-road-inspired "boxy" SUVs (often referred to as "soft off-roaders"). These vehicles emphasize rugged aesthetics, camping utility, and spacious interiors.

However, the study warns that these segments are particularly vulnerable to quality pitfalls. While their design drives strong initial interest, their physical attributes create engineering challenges:

NVH (Noise, Vibration, Harshness): The boxy aerodynamics and larger tires of off-road-style SUVs inherently generate more wind and road noise. Without meticulous sound deadening, this degrades the "premium" feel consumers expect from EVs.

Ride Comfort: Balancing the suspension for "rugged" looks versus city driving comfort is proving difficult, leading to complaints about ride quality.

The data indicates that while emotional appeal drives the purchase, the reality of living with a noisy or uncomfortable vehicle erodes long-term satisfaction. If these "lifestyle" models cannot master the basics of NVH and ride comfort, their market momentum could stall despite their visual popularity.

The Price War Effect: 10–30万元 Segment

The fiercest battleground for quality is the 10–30万元 price range.

PHEV market share in this bracket grew by 8 percentage points year-over-year.

EREV market share in the 20–30万元 bracket gained 3 percentage points.

This mass-market segment is extremely price-sensitive and volume-driven. The data suggests that the "Price War" in China—where manufacturers aggressively slash prices to gain share—may be contributing to the quality dip. Cost-cutting measures, combined with shortened development cycles to pump out new models, are manifesting as the design flaws and software glitches recorded in the study.

Part V: Strategic Implications and The Way Forward

From "Tech Stacking" to "Experience Value"

The overarching theme of the 2025 NEV-IQS is a critique of the industry’s current product philosophy. Yang Tao, General Manager of J.D. Power’s Automotive Product Division in China, provided a sharp assessment of the situation:

"In the early phase of smart feature proliferation, there was heavy stacking of technology. Now, the industry must return to the essence of user experience value."

This concept of "Tech Stacking"—marketing vehicles based on the number of sensors, the size of screens, or the theoretical speed of chips—has yielded diminishing returns. Consumers are no longer impressed by features that exist only on a spec sheet; they demand features that work reliably in daily traffic.

The New Mandate for Automakers

To reverse the trend of rising PP100 scores and regain consumer trust, the report outlines a clear strategic roadmap for automakers, particularly those dominating the PHEV and EREV spaces:

Software Stabilization: The "shoot first, patch later" mentality of OTA (Over-the-Air) updates must be curbed. The initial release of infotainment systems must be robust. Automakers need to invest as much in UI/UX testing as they do in battery safety.

Hybrid Refinement: For PHEV and EREV manufacturers, the focus must shift from simply achieving high range figures to ensuring the seamless integration of the dual powertrains. Reducing fault rates in EREVs is an urgent priority.

Restoring Physical Controls: The rise in control-related complaints suggests a need for a hybrid interior design—one that balances touchscreens with physical tactile controls for critical functions, ensuring safety and ease of use.

NVH Mastery: As the market shifts toward boxy SUVs and lifestyle vehicles, mastering the acoustics and vibration dampening of these non-aerodynamic shapes will be a key differentiator between premium and budget perceptions.

3

Notable Performers

Despite the general headwinds, the study highlights that quality leadership is still possible. Models like the Li L9 (in the luxury EREV SUV segment) and the BYD Seagull 06 PHEV (in the mainstream PHEV sedan segment) were recognized for their performance. However, even these segment leaders operate within a market where the average quality bar is slipping. Their success lies in managing the trade-offs better than competitors, but they are not immune to the industry-wide struggle with digital integration.

Conclusion

The findings of J.D. Power’s 2025 China NEV-IQS serve as a vital reality check for the world’s most dynamic automotive market. The industry has successfully conquered the "hardware" phase of the NEV revolution, delivering batteries and motors that are efficient, long-lasting, and capable of alleviating range anxiety.

However, the industry has stumbled into the "software" phase. The sharp rise in infotainment complaints, the reliability issues plaguing complex hybrid powertrains, and the deteriorating usability of vehicle controls send a clear message: Innovation without reliability is not progress; it is friction.

As sales of PHEVs and EREVs continue to surge, and as digital cockpits become ubiquitous, the winners of the next phase will not be the brands with the biggest screens or the most complex powertrains. The winners will be the automakers who can "return to the essence," delivering a driving experience that is not just technologically advanced, but intuitively usable and fundamentally dependable. In the eyes of the 2025 consumer, a glitch-free screen has become just as valuable as a long-range battery.